The new Montana Board regarding Homes mortgage program which is most readily useful to you personally relies upon several points like credit rating, personal debt rates, income additionally the purchase price in your home. He is the best resource to answer questions and to meet the requirements a purchaser for a financial loan. Be sure to let them know need good Montana Board away from Casing financing.

Money always purchase funds come from taxation-excused bonds titled Mortgage Revenue Bonds, or MRB's, and also the Internal revenue service (IRS) enjoys seven qualification standards all consumers have to be considered under:

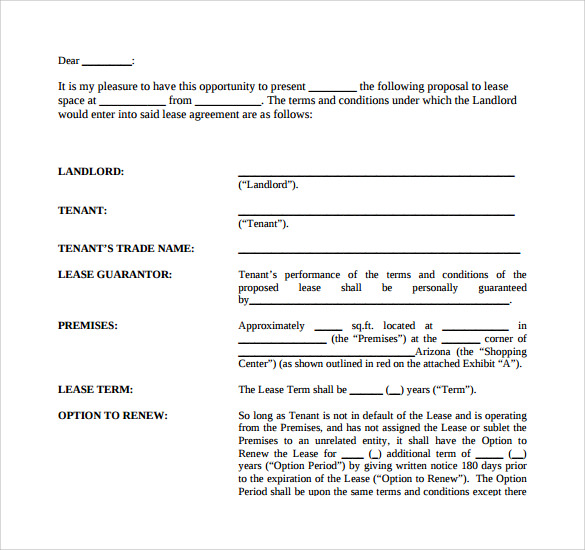

- Earnings Limits

- Price Restrictions

- This new household need to be a good borrower's primary quarters

- Exchange loans in Lakeside otherwise company play with do not exceed 15% of one's residence's complete area

- Feel a primary-big date homebuyer (perhaps not owned a primary quarters into the earlier around three-age, *some exclusions apply)

- Loans is employed to get a house (zero refinancing finance)

- Recapture Taxation are a possibility

Financial Apps

Regular Thread System try a 30 12 months, low-rate of interest loan and that's aimed toward basic-time homeowners when its income and get pricing is beneath the released restrictions. This option has income restrictions considering most of the members of the household 18 and you will more mature. Our home is available any place in Montana and you will includes single loved ones property, apartments and are built house. To be eligible for Montana Panel out of Property software, an excellent homebuyer have to earliest be eligible for a keen FHA, Va, RD otherwise HUD-184 first mortgage loan.

Down payment Advice otherwise a great "Subordinate Loan" will likely be alongside any one of all of our financing programs to help homebuyers which have funds necessary to get a property. If the cash at the closing is your problem, an effective Montana Board out of Homes Down payment Guidance 2nd Home loan normally assist. Find out more right here.

Unique Software are created getting homeowners exactly who discover deposit direction or qualify for apps offered by low-payouts, regional governments or any other partner communities which were approved by new Montana Board out of Property. These include Environment to own Humankind, Community Land Trusts and you can NeighborWorks. This type of communities generally require borrowers becoming in the or lower than 80% off area median money. These special applications give earliest mortgage loans from the significantly lower rates to target populations to eliminate traps so you're able to homeownership.

80% Shared System provides homeowners that eligible for Montana Board from Construction financial support having a substitute for an FHA-insured financing, reducing the necessity for home loan insurance coverage. The 80% Joint Program is actually a thirty-season very first-reputation real estate loan during the 80% Loan-To-Well worth (LTV) that's combined with an extra mortgage on 20% Loan-To-Worth (LTV) given by a partnering non-earnings.

Home loans

Montana Veterans' Home loan Program brings first mortgage funds to Montana people providing otherwise who have supported from the armed forces through the government armed properties and the Montana National Guard. Program financing are given about dominating of one's Montanan Coal Tax Believe Finance; income and buy speed limits dont pertain. Montana Panel regarding Property administers the application form, to your Montana Panel off Financial investments (MBOI) purchasing the mortgages. The loan interest try step 1% lower than market and helps qualified Veterans pick its first home. Excite talk with your Performing Financial on almost every other limits that will use.

Financial Credit Certification , labeled as an enthusiastic MCC, is actually a buck-for-dollar taxation credit that reduces the number of government income tax paid off by a primary-day homebuyer. This new taxation borrowing is equivalent to 20% of one's home loan interest (to not exceed $2,000) repaid inside the tax seasons. Below this choice, this new homebuyer selects and links the fresh federal income tax borrowing from the bank in order to a mortgage loan; Montana Panel out-of Homes finance commonly qualified to receive MCC. The brand new homebuyer need meet with the exact same Irs qualifications requirements since the Montana Board out of Housing loan apps. Lenders may use it income tax borrowing to help be considered the buyer to the financing. It's important to understand that this is certainly an income tax borrowing from the bank and never a loan.

Financial Borrowing Certificate (MCC) Re-Issuance : Whether or not a borrower just who receives an MCC refinances the home mortgage, Montana Panel of Homes will get, but is not as much as zero obligation, elect to re-procedure including MCC according to the fine print as the set forth throughout the Mortgage Borrowing Certificate Guide. However, the MCC might possibly be reissued on the amortized balance of one's modern loan, even if the loan amount is improved in the re-finance.

No Comments